Canadian Non-Residency Withholding Requirements

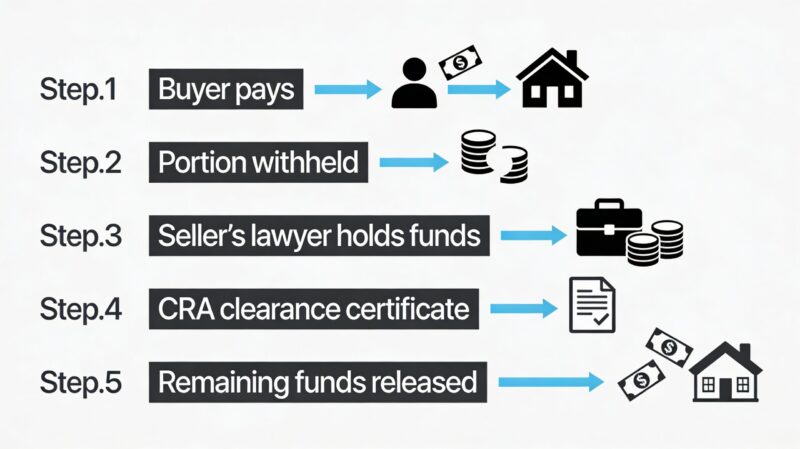

When a seller is a non-resident of Canada for tax purposes, one issue immediately comes into play that can significantly impact closing: a mandatory withholding requirement. A portion of the purchase price must be withheld unless the seller provides a clearance certificate from the Canada Revenue Agency, and if that step is missed, the buyer can be held liable for the seller’s tax.

That withholding is often misunderstood. It is generally calculated on the gross purchase price, not the seller’s net proceeds. In many cases, that means 25% of the purchase price is held back, and potentially more depending on the type of property.

For example, on a $600,000 sale, the required holdback may be $150,000, even if the seller only expects to net a fraction of that after paying out their mortgage and closing costs. If there is insufficient equity to fund the required holdback, the seller will be required to make up the difference at closing to satisfy this obligation.

The Legal Framework

This obligation arises under the Income Tax Act (Canada) and places the responsibility squarely on the buyer to ensure the required amount is withheld and remitted.

If the buyer fails to do so, the buyer is deemed liable to the Canada Revenue Agency for the seller’s tax liability, up to the amount that should have been withheld. In practical terms, the buyer can end up paying the seller’s tax bill.

Why This Exists

This is not a procedural technicality. It is a risk allocation mechanism built into the legislation. The CRA has limited practical ability to enforce tax collection against a non-resident after the proceeds leave Canada, so the statute shifts that risk upstream to the buyer at closing.

It is important to understand that the withholding is not the final tax. It is a security against it.

How It Actually Works in Practice

While the legal obligation rests with the buyer, the holdback is typically implemented through the seller’s lawyer. The seller’s lawyer will give an undertaking to retain the required funds from the sale proceeds and deal with the clearance certificate process. This structure allows the transaction to close while still protecting the buyer from statutory liability.

Once the seller obtains a clearance certificate confirming the actual tax payable, the appropriate portion is remitted to the CRA and any excess is released to the seller. While timelines vary, the clearance certificate can take months to issue after closing, meaning the seller’s funds are tied up for a significant period of time.

Where Deals Get Into Trouble

From a deal mechanics perspective, the issue is rarely the rule itself. It is timing and expectations. If non-residency is identified late, sellers may be expecting significantly higher net proceeds, there may not be sufficient equity in the transaction to support the holdback, and the parties are left trying to rework the deal under time pressure.

From a liability standpoint, the buyer has very little flexibility. If there is no clearance certificate, withholding is the default position. It is not meaningfully negotiable because the statute attaches the risk directly to the buyer.

Final Takeaway

Non-resident sellers do not usually change the legal structure of a transaction. They change the financial outcome and the risk profile.

The takeaway is simple. The withholding requirement exists to protect the CRA, but it operates by placing the compliance burden and potential liability on the buyer, even though in practice the funds are usually held and administered by the seller’s lawyer. Identifying this early keeps the transaction manageable. Identifying it late is what creates pressure at closing.